Last week Rachel Slaymaker, in the ESRI’s Spring Economic Commentary, summarized the options in terms of potential RPZ reform. With this as a point of departure, and given the Housing Agency’s review of RPZs should be submitted by now, I look at all the options on the table, there strengths and weaknesses and what we are likely to see (at the end I include a table summarising all options and their pros and cons). This post goes out to paid subscribers fist and to all subscribers on 07/04/25)

The ESRI’s just published Quarterly Economic Commentary includes a summary of what we know about the impacts of RPZs (see my extended summary of the evidence and issues here). Within RPZs, ongoing tenants on average experienced annual rent increases of between 1.3–1.5% in Dublin and 1.4–1.7% elsewhere. This compares to average property level rent inflation outside the RPZs of 3.5–4%. Moreover, rent increases between tenancies were 2.8–3.2% in Dublin, and 14–16.4% outside the RPZs This is quite remarkable considering that non-RPZ areas are generally rural or small towns at this stage, and have no where near the level of demand Dublin sees. The conclusion is that ‘RPZs have had a clear impact in limiting the rental inflation households have faced’ and that they ‘have been broadly effective in relation to their aim of limiting rent increases for properties in designated areas’.

On the other hand, there are a number of negative effects:

Average rents paid by new tenants are significantly higher (around 15%)

The number of new tenancy commencements has been trending downwards since 2010, suggesting decreased mobility. (I would argue, however, that given one objective of rent regulation is to deliver more stable tenancies, lower tenancy turnover may actually be a good sign)

Gillespie et al.’s research finds that RPZs increased the supply of homes for sale and reduced rental listings, but that this only relates to small-scale landlords after the 2% caps came in 2021

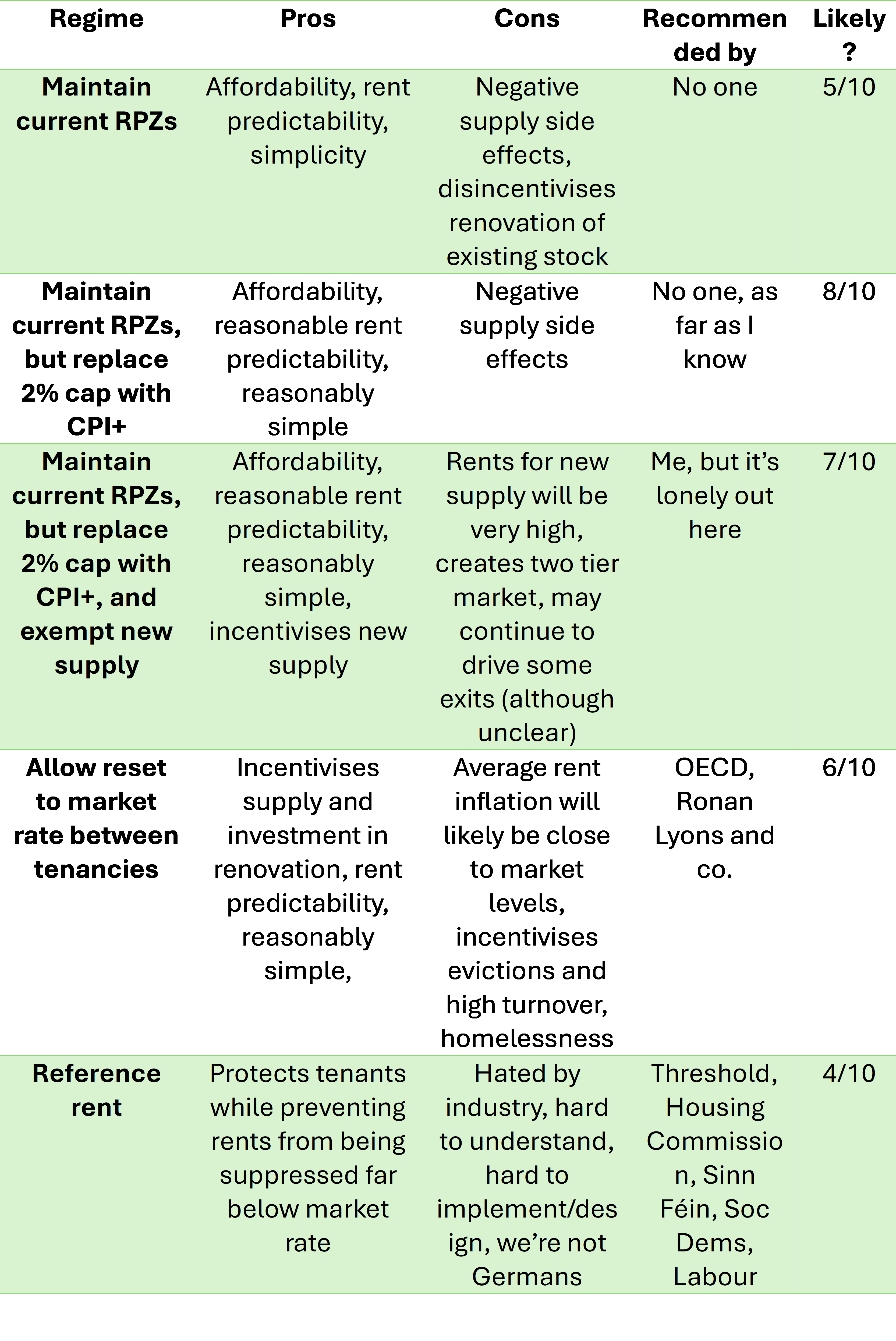

Slaymaker goes on to assess three potential options for reform:

Continue with the RPZ model but extend it to all PRS tenancies, and link the cap to some meaningful index.

Coffey et al.’s earlier work raises the possibility of linking rent increases to something like the Consumer Price Index (CPI) + x per cent. This approach would continue to give rent stability and some affordability gains to tenants, while hopefully not unduly undermining investment/supply. However, it could lead to some rents falling significantly below market rates over the medium to long term, which is one of the problems with the current regime.

Cap rent increases within tenancies but allow rents to reset on turnover

This would allow rents to return to market rents at intervals, but the obvious problem is that the affordability impact would be minimal ‘if rents are regularly resetting to market rates’. As tenancy turnover is typically high (I believe the average tenancy lasts a year or two - if anyone has clear data on this please let me know), my own view is that this form of regulation is tantamount to complete deregulation in many respects, and we would likely see much higher rates of rent inflation. Moreover, as I also argued on the Inside Politics podcast, Slaymaker notes that ‘it would favour landlords with frequent turnover of tenants’ and incentivize evictions. This could of course undermine the Government policy objective of reducing homelessness. Slaymaker notes that consequently, such a measure would likely require enhanced security of tenure protections, although my views is that given non-compliance and other issues even this would not fully address the downsides.

Reference rents

This would involve linking the setting of initial rents and rent increases to an index based on average rents in similar properties at a local level. From a tenants’ perspective, this is probably the best option, and it is the model used in what are arguably the two most pro-renter European countries (Netherlands and Germany). But it suffers, as Slaymaker notes, from feasibility issues. Specifically, she argues that it is:

Complex for tenants and landlords

Unclear how to calculate reference rent

Has challenging data/implementation requirements

I’ve been chatting to various people about these issues (in industry and policy) over the last while, and there appears to be huge push back on this idea from industry and concerns about the feasibility from policy makers.

Another option (which could be added to any of the above), not discussed in the ESRI paper, is to exempt new supply from rent regulation altogether, or for a defined period of time. Under the current RPZ regime, ‘new properties’ are defined as properties which have not been rented in the previous two years and, while initial rent setting is not regulated, subsequent rent setting is regulated under the 2% cap.

I’ve never understood this definition of new properties because including second-hand units does nothing to enhance construction, and hence the actual supply of housing, and simply incentivizes the redistribution of property from the owner occupation to private rental sector. Indeed, it is quite possible that under the current system there are landlords selling properties to homeowners to escape below market rents, while conversely owner occupiers are selling properties to landlords who can then set rents at market rates. What the policy win here might be is a mystery to me. Moreover, although new properties are regularly described as ‘exempt’ from the RPZs, they are in fact subject to the 2% cap for all subsequent reviews.

If the objective is to incentivize genuinely new supply, it seems to me that the logical route would be to fully exempt newly constructed units (i.e. units constructed after a given date would remain entirely unregulated), at least for a period (say, ten years). In Demark, for example, rents for properties built after 1990 are much more weakly regulated. Given the main concern with RPZs appears to be the fall in apartment supply from the Build to Rent sector this seems like an obvious move, and it would not effect existing tenants and would also not have a huge impacts on average rent inflation as new units represent a small portion of the overall market. (The caveat here is that high levels of BTR might have unintended consequences for other parts of the housing system, e.g. declining homeownership, gentrification, over-reliance on international capital, etc.).

So, considering the pros and cons as well as the realpolitik, which of the above are most likely? Below I evaluate a number of hypothetical scenarios from the perspective of Government’s stated policy objectives (as opposed to my own views):

Scenario 1: Fianna Fáil and Fine Gael wake up one morning and remember what being a centre-right party actually means

With two centre-right parties in power which claim to be concerned with supply, it seems obvious that the new rent regulation regime should allow rents to be reset to market. The obvious way to do this is the second option discussed above: allow rents to reset to market rate between tenancies. Maintaining rent regulation during tenancies would provide some political cover, and the core supply-side problems with the RPZs would be definitively solved. This form of rent regulation, moreover, is easy to understand and administer, and therefore doesn’t raise any policy design/implementation challenges. Moreover, it has been recommended by the OECD and also in this opinion piece by Ronan Lyons, Michael O’Flynn and Dermot O’Leary.

In reality, however, since 2016 the one consistent feature of PRS regulation is that it has always tended to be surprisingly pro-tenant. Back in 2016 I didn’t expect the introduction of RPZs, and I certainly didn’t expect their further tightening or that they would still be here 9 years later. Fine Gael have been making lots of pro-tenant noises already in the context of the RPZ reform debate (bizarrely for a party which likely garners a lot more support from landlords than tenants). So I think this scenario is very unlikely. In my view, if we were to go this route rent inflation would become a major political issue within a few years and we’d end up with further regulating, thus adding to the ‘policy certainty’ issue.

Scenario 2: The Government goes for reference rents, despite the feasibility challenges

In terms of affordability, reference rents have a lot to recommend them. They have been recommended by Threshold, as well as the Housing Commission, Sinn Féin, the Social Democrats and Labour. They would also prevent rents from falling unduly below market rents, and therefore would address at least some of the supply-side concerns.

The problem is that industry hates them and they would be technically difficult to design and implement. At the risk of being unfair, I get the impression that few people, either in policy making or in industry, believe that Ireland is capable of effectively implementing such a system. The fear is that we end up with something that is incomprehensible, arbitrary and disincentivizes investment from both small-scale and institutional landlords. Despite the fact they (again bizarrely) have been mooted by the Taoiseach on numerous occasions, I find it hard to imagine reference rents being implemented, at least within the next couple of years, mainly due to the implementation challenges and related possibility it could go badly wrong. So I would say this scenario is also very unlikely. (As an aside, Spain have recently introduced temporary rent controls which will be replaced by a yet to be specified reference rent systems in 2027).

Scenario 3: The new policy reflects the interests of tenants and is based on a robust understanding of the PRS, and its relationship with wider Government policy objectives

From a tenant point of view, the best option (in my view) is probably maintaining the current system but either returning to 4% caps or linking the cap to HCPI, combined with an exemption for new supply. This should maintain almost all the affordability and predictability benefits of the current regime, while sending a very clear signal to the Build to Rent sector and thus facilitating new supply of the type most needed (one and two bedroom apartments in high demand areas).

This also has the benefit of requiring minimal legislative change, being clear for tenants and landlords, and not creating any new implementation/regulation challenges. Politically, it would be fairly effective in insulating Government from opposition attacks of ‘throwing tenants under the bus’ etc. The most politically unpalatable part of this suggestion is the exemption of new supply.

As noted above, in my view the recent past suggests that the new regime will be err on the pro-tenant side, so I don’t think we’ll see a move to deregulate between-tenancy rent increases (unless the Taoiseach was serious when he talked about ‘pivoting’ to a more pro-market position). This is possible given many political commentators believe Michéal Martin wants to ‘put his stamp’ on this administration and ‘leave a legacy’, which suggests we may see some surprising developments).

Because of the feasibility issues, I also don’t think we’ll see reference rents. Therefore, I think we will see the continuation of the current regime but with either 4% or CPI+ caps, and with an outside chance that new supply will be exempt within a specified time period. I expect it to be introduced in December 2025 (i.e. when the RPZs expire under the current legislation).