Irish housing: crisis or transition?

The Week in Housing 01/03/22

It was sad to see the recent passing of Peter Marcuse, an inspirational radical planner who, among other things, wrote one of the books that my students read every year – In Defence of Housing. One of his quotes that was doing the rounds on Twitter following news of his death was:

“Homelessness exists not because the system is not working, but because of the way it works”.

This got me thinking about the Irish housing ‘crisis’. To what extent should we think of what is happening in the Irish housing system as a crisis? Describing the current malaise in this way risks letting the ‘the system’ off the hook, because it suggests that the system itself would lead to desirable outcomes if it were not currently ‘in crisis’. As the Marcuse quote above indicates, there may be a danger of treating issues like high house prices or evictions as a bug, when they are in fact a feature of our housing system. That is one line of thinking anyway.

But even on a more analytical level, does the term crisis obscure more than it reveals? Today, I want to argue that a lot of what is happening might be better understood as a part of a ‘housing system transition’, in that it is a consequence of the emergence of a new set of structural forces within the Irish housing system, rather than simply the breakdown of the previous structures. Indeed, part of what makes are current predicament so complex, and so seemingly intractable, is precisely that it is a mix of both crisis and transition elements.

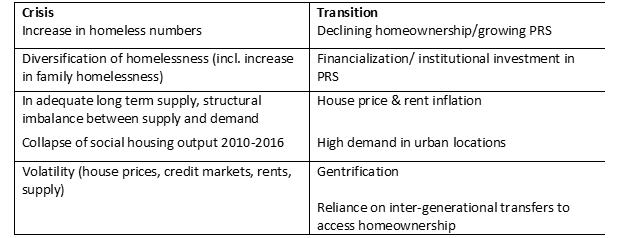

Below I look at which elements of our ‘housing crisis’ should be considered as ‘crisis elements’ and which elements are better understood as part of the above mentioned transition.

Let’s start with the latter. We can begin to think about the ‘transition elements’ via the international ‘post-homeownership society’ and ‘financialization of housing’ literatures. The former (see this article by Forrest and Hirayama and this one by Ronald and Kadi) tend to focus on the transformation of housing policy since the 1990s. As states have withdrawn from the provision of social housing and, more importantly, supporting access to homeownership (e.g. subsidised/public mortgages; protected mortgage lending institutions; mortgage interest relief; grants; tenant purchase etc.), homeownership has become intensely commodified. This, combined with less favourable labour market conditions (precarity etc.), makes it harder for working class and middle-income households to access homeownership, especially early in life.

The ‘post-homeownership society’ is characterised by both generational and class inequality (something I discussed before here). It involves the concentration of increasingly valuable residential real estate assets among fewer households (class), as well as advantaging the boomer generation which enjoyed historically favourable conditions for accessing homeownership, and can leverage this to acquire additional properties or give gifts/inheritance to their children (generational).

The financialization literature is a little more unclear in terms of what type of housing system we are moving to, but the main features are high and volatile house prices, the concentration of ownership of residential property among financial institutions, and gentrification.

These are two important bodies of literature, but they leave out some really important issues. The two main ones I would point to are demographic change and economic/labour market dynamics. Demographic change mainly impacts in the form of far more one person households over time and far more older households. Migration is also an important factor.

Economic/labour market change is particularly important in the Irish context. Here I have in mind two main features. The first is labour market polarisation associated with the type of service sector we have developed. To put it bluntly, those in low and middle-income jobs cannot compete with high earning professionals in finance, advanced professional services, tech and law. To my knowledge, we do not have any specific research documenting this in the Irish context, but there is research internationally showing that income inequality leads to restricted access to housing for low-income households.

The second (and related) factor is the concentration of high-paying service sector jobs in central urban locations, i.e. the Docklands and Dublin 2. These two factors combine to create huge housing demand in ‘core Dublin’, i.e. the parts of Dublin which are located close to the areas of high-paid jobs. Again I am not aware that there is any research looking at this directly in Ireland, but Hulse and Yates writing about the Australian context certainly resonates:

An uninterrupted period of economic growth since the mid-1990s, associated with structural change away from manufacturing and towards a service-based economy, has imposed unprecedented pressure on Australia’s urban housing markets. Jobs and population have become increasingly urbanised with high-paying jobs being concentrated in city centres. The central business district (CBD) has become a ‘jobs magnet’ with the shift from labour-intensive industrial production often in outer suburbs to centrally based knowledge-intensive industries relying on high job densities for their productivity. By 2011, the densities of jobs in the centres of both Sydney and Melbourne, at more than 4000 jobs per square kilometre, were more than 100 times greater than in the outer regions of each city.

There is one final transition factor which is important to note. There appears to be a kind of cultural/generation change in terms of housing preferences among middle-class and upper-middle class households. Again there are two elements. First, the gentrification story – prospective home buyers are increasingly interested in living in more “interesting” parts of cities (i.e. formerly working class) and are not as concerned with having a prestige address, posh schools, big gardens and driveways, and a near-by golf club. For reasons best known to themselves, this new generation are mainly interested in well-known favourites such as hipster cafes, pubs “with character”, frowning at SUVs and so on. Second, there is a ‘quality of life’ preference, turbo charged by the pandemic, which is likely to see a focus on formerly working class small towns and villages in rural Ireland which are commutable to Dublin but offer access to natural amenities, more ‘quality of life’ and [*shudders*] sea swimming. Somewhere like Wicklow Town would be a prime example here. This phenomenon can be empirically observed by the prevalence of ‘dry robes’.

Hulse and Yates summarise the international literature on such ‘lifestyle effects’, involving:

… [T]he movement of middle and higher income families with children into inner-city areas as part of ongoing gentrification of these areas. Detailed research into changing family lifestyles has suggested that some of the drivers are the need to combine work and care, aspirations for children’s education and new practices of family consumption in resource rich areas of the city.

There are lot of different trends touched on above, encompassing housing policy, financial markets, labour markets and demographics, but taken together it can be argued that they represent a transition to a new housing system which has several key features:

· House price inflation, very high demand in urban/desirable locations

· Concentration of ownership of residential property

· Declining homeownership

· Gentrification

Obviously, the consequence of all of the above is less affordability, more renters, more insecurity, evictions and displacement of working class and lower income households.

Although the evidence in the Irish context is limited, and therefore the above is somewhat speculative, it seems to me the above ‘transition features’ are important and very much overlooked in the current debate.

The above notwithstanding, it is very important to note that some important elements of housing in Ireland are best understood as ‘crisis features’. To my mind, these features can best be identified by focusing on the immediate consequences of the 2008 crash and subsequent years of austerity. The two key features both relate directly to supply. First, long-term, structurally low levels of private market housing supply (arising from the banking crisis, volatility in relation to credit availability etc.). Second, the collapse of social housing supply between roughly 2010 and 2018 (and related shift to HAP).

The most direct consequences of these ‘crisis features’ include the further undermining of homeownership, growth of the PRS, and very high levels of homelessness, as well as the ‘diversification of homelessness’, i.e. more homeless families etc.

Part of what makes the ‘Irish housing crisis’ so difficult to understand and so intractable is that it is in fact a confusing combination of crisis and transition. Moreover, while the ‘crisis features’ are well understood and have been documented in the Irish academic literature, the ‘transition features’ are not as well understood nor have they been particularly well documented. This is concerning because, in the long run, the transition elements may prove to be the more consequential, and this may mean the challenges in our housing system are even deeper than we realise.

Events

A very exciting new report on land speculation and housing by TASC is being launched on April 7th. Details of this year’s Conference of Irish Geographers have also been announced, it will take place in Limerick 18th-20th of May.

What I’m reading

A fascinating new report from the Jesuit Centre for Faith and Justice on cost rental was published this week, definitely a must read, as was a very important international study looking at the impact of Covid-19 and related public health measures on housing. On the podcast front, there was an interesting discussion of ‘tools to combat financialization’ with Michelle Norris and Julie Lawson on the Housing Europe Podcast.