Are RPZs killing apartment supply?

The Week in Housing 14/03/15

Today’s post is a bit longer than usual, but it challenges the prevailing narrative that RPZs are undermining Build to Rent apartment supply and thus addresses a crucial policy/political issue. Detailed posts like the below take a fair bit of work and are made possible by paying subscribers, so thank very much to everyone who has signed up. Don’t forget to register for the first of the Webinar series I’m organising (Darren Baxter Clow on the topic: 'Can bringing private homes into social ownership rewire the housing system?')

The decline in housing supply in 2024 has been the biggest issue in housing politics so far this year. The Government’s claim that we would see 40,000 new units turned out to be misleading. But as the old saying goes, never let a crisis go to waste. Micheál Martin quickly performed a rhetorical pivot that framed the RPZs as the culprit for the disappointing supply figures, arguing that they do not create ‘a clear, stable environment in which to invest’. This take was bolstered by the fact the construction of Single Family Dwellings and Self Builds remained stable in 2024; the decline in apartment construction was responsible for the overall lower output.

Industry and commentators quickly seized the opportunity, with a flurry of criticisms emerging around the RPZs.

Ronan Lyons, Michael O’Flynn and Dermot O’Leary wrote this opinion piece in The Irish Times arguing that:

“Ireland was not the only country to have seen a fall in the construction of private rented sector stock during the period of higher interest rates of recent years. But with RPZs tightening considerably in 2021, the fall in Ireland has been greater than elsewhere, showing the impact that poorly thought-out rent controls and policy uncertainty can have on supply”.

(As an aside, apart from the fact that O’Flynn in particular has a direct economic interest in rent deregulation, it is quite remarkable that three members of the Housing Commission embarked on this solo run to undermine the findings of the report they themselves had been involved in writing).

Irish Institutional Property, in a post on LinkedIn, said ‘In the absence of decisive government action without further delay to reform the current rent cap this trend [declining investment] will only worsen’. Pat Farrell, CEO of Irish Institutional Property, in a letter to the Irish Times, wrote that ‘Rental prices began to climb again in 2024 in tandem with a marked reduction in new supply, as the impact of the 2% rent caps continued to bite, resulting in institutional investment drying up’.

Hooke and McDonald (estate agents and property consultants) argued in their recent report that the fall off in apartment supply was ‘directly attributable to the rent cap which is killing supply in the rental market’.

At no stage have I seen anyone cite any evidence that there is a causal connection between RPZs and the decline in supply. Nevertheless, this argument was, largely uncritically, picked up by the media and is now shaping the debate on the reform of the rental sector.

But what if the claim that RPZs have undermined supply is just as misleading as the fabled 40,000?

I’ve been in the media a bit discussing RPZ reform and have argued that three factors are at stake in the decline of Build to Rent (BTR) output: interest rate hikes, construction cost inflation, and the RPZs. Over the last week I’ve been doing a bit of digging into the international data to get a better understanding of the role of these different factors, especially trying to untangle the respective impact of interest rate hikes and RPZs.

Most advanced economies have a BTR sector, and all of them experienced interest rate hikes just like Ireland (as well as construction cost inflation). Some of those countries have housing systems fairly similar to our own, but don’t have rent regulation. So we can get a clearer understanding of the impact of interest rate increases in the absence of rent regulations.

Let’s remind ourselves of the issues in our own BTR sector before looking at international examples. Apartment completions fell from 12,000 to 9,000 between 2023 and 2024 (virtually all apartments in Ireland are delivered via institutional investors). A 25% decline is of course very significant. Commencement notices fell by about 4,000 between 2021 and 2022, but increased again in 2023 and 2024, however we should note that the commencement data is not, in the Irish case, a reliable predictor of supply.

Now let’s look at world’s largest BTR market: the US. Over there the sector is called ‘multifamily’ and has been well established for decades. Although there is quite a lot of variety, most cities in the US don’t have rent regulation, and even those that do have much more liberal regimes than our own RPZs. Cushman and Wakefield’s data (see figure below) on US Multifamily shows that:

“Developers are pulling back significantly, with just 230,000 units breaking ground in 2024—on par with 2012 levels and over 30% below the pre-pandemic (2017-2019) average of 330,000. Most forecasters project 2025 deliveries will be roughly half the rate of 2024.” (my emphasis)

So, the US has seen a massive decline in BTR investment and construction, indeed much more significant than our own.

The UK is more similar to Ireland, both in terms of its overall housing system and in that BTR is a new sector which took off post-financial crisis. The one big difference is that it is the most weakly regulated rental sector in Europe. If we want to look at how BTR investment performed in a country which has neither rent regulation nor security of tenure, we need look no further.

And, lo and behold, what do we find only that BTR investment has plummeted there too (see BTR starts in the below figure).

The above data is from this report from British Property Federation. UK BTR units under construction collapsed from over 25,000 units in 2022, to under 10,000 in 2024.

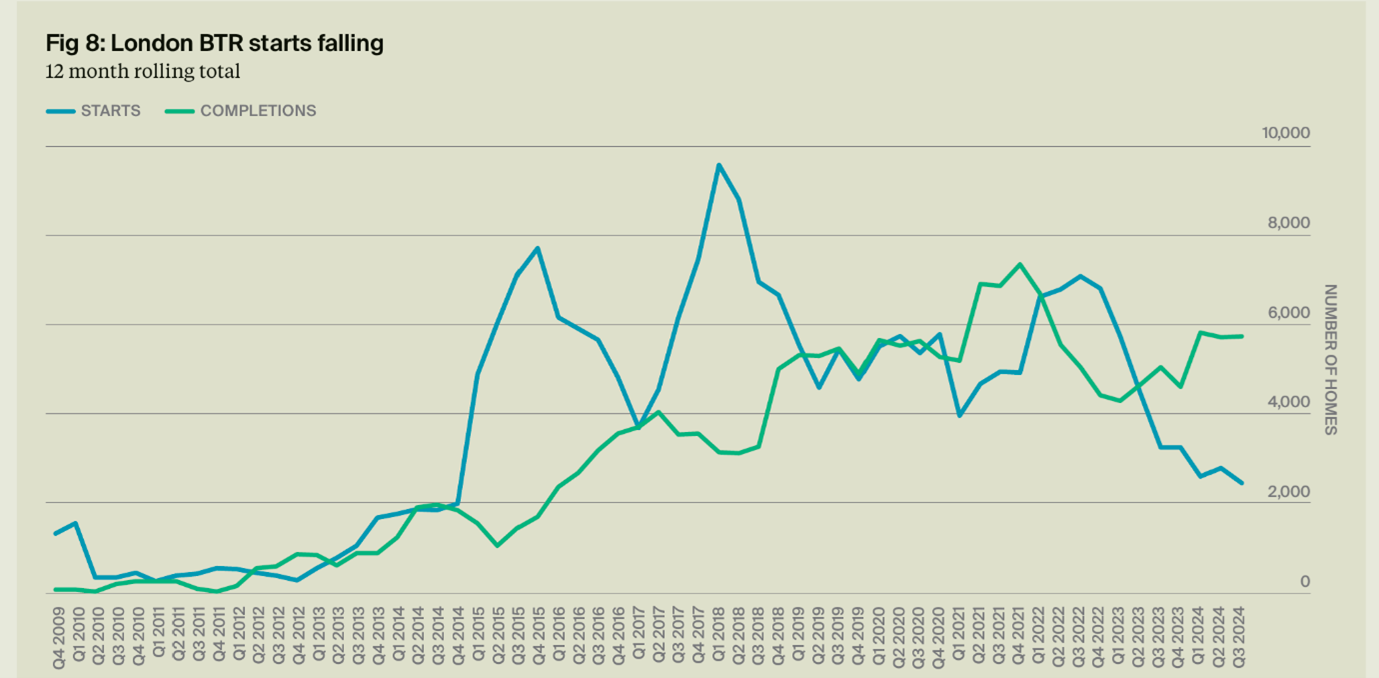

This Knight Frank report shows that the picture in London was even worse, with new BTR starts declining to the lowest annual level since 2014 (see BTR starts in the figure below).

The UK and US are usually grouped with Ireland as so called ‘Anglo Liberal’ housing regimes. However, they are of course not in the Eurozone. Although both the Federal Reserve and Bank of England increased interest rates over the same period as the ECB, their interest rates were slightly higher. It is therefore instructive to look at some of our European neighbours. Germany is by far Europe’s largest BTR market, as more than half of households are renters. It does have rent regulation, but this regulation is (a) arguably more lenient and flexible than Ireland’s and (b) didn’t stop a BTR investment boom when interest rates were low.

So, based on the prevailing wisdom in Ireland, we would expect German BTR investment to have performed better than in Ireland over recent years. Nothing could be further from the truth. In fact, the decline in BTR has been of a much greater magnitude in Germany than in Ireland. According to CBRE, in the first half of 2023, ‘the transaction volume in Germany’s investment market for multifamily properties (upward of 50 units) came in at €3.1 billion, marking a decline of 61 percentage point compared with the year-earlier period’. This data relates to total investment volumes, rather than investment in new supply. Looking at forward funding transactions (also one of the main forms of funding BTR in Ireland), ‘in the first half-year of 2023, €965 million was allocated to forward funding transactions as against €3.1 billion a year ago’.

Based on this brief overview, it appears that Ireland has actually outperformed the UK, the US and Germany in maintaining BTR supply in a context of interest rate hikes. The conclusion can only be that interest rates have played a decisive role in ensuring BTR supply has fallen in jurisdictions irrespective of their rent regulation policy.

To be clear, I am not claiming that RPZs had absolutely no impact. Investment decisions are a function of the relationship between interest rates and expected rental growth (I’m oversimplifying but these are the basics), so RPZs of course play a role in investment. But there is certainly no evidence that RPZs are the decisive factor. The evidence presented above strongly supports the argument that interest rates were the decisive factor.

Stepping back from the data, let’s consider how the demonization of RPZs was able to take hold in Irish debate so quickly. It seems to have worked something like this:

- The decline of overall housing output put the supply question front and centre

- Michaél Martin’s intervention framed the issue around RPZs and institutional investment

- Mitchell and McDermott’s report, which received a lot of attention in the media, showed that the fall off in supply was related to the decline in apartment construction, which as noted is virtually all institutionally funded

- Various stakeholders, including industry (funds, developers, estate agents etc.), jumped on the opportunity to frame RPZs as the main cause

- The media and politicians then accepted the claims of industry, without, it appears, subjecting them to much in the way of scrutiny.

To my knowledge, none of the critics of RPZs, nor any of the politicians, have been asked to provide concrete evidence of the claim that RPZs are causing a decline in apartment construction.

Over the past few weeks, I have met numerous people involved in these debates who have said words along the lines of ‘I speak to developers all the time and they tell me RPZs are a huge problem’. This is simply not a credible argument, and certainly not one policy should be based on.

It was not at all difficult for me to find holes in the arguments made against RPZs. If I was able to do this, you can be damn sure that everyone involved in institutional funds has known this for a long time. What bothers me most about all this is how high the stakes are, especially for tenants. The quality of our debate really matters.

Events & News

Myself and Sarah Sheridan are organising this series on ‘Making rental housing affordable’:

Wed 19 March (1-2pm): Dr Darren Baxter (UK) - Can bringing private homes into social acquisition rewire the housing system?

Wed 16 April (1-2pm): Dr Gerald Koessl (Austria)- Cost Rental Housing in Austria: How does it Work and What is the Impact on the Housing Market

Wed 21 May (1-2pm): Solveig Raberg Tingley (Denmark) - Non-Profit and Affordable Housing: The Danish Experience

Wed 11 June (1-2pm): Dr Eduardo González de Molina (Spain) - Rent Regulation in Spain

Wed 25 June (1-2pm): Prof Stefan Kofner (Germany) - Critical Analysis of the German Local Reference Rent System: Challenges and Perspectives

Also, the Housing Ireland conference is happening next week. Great line of speakers but sadly I can’t make it.

What I’m reading

Really looking forward to reading this newly published report (funded by Housing Agency) on migration and housing needs, by Valesca Lima. Another new book on radical tenant politics. Interestingly (at least to me), this is the fourth book on this topic written over the last two years, the others being Abolish Rent, Against Landlords, and one (only available in Spanish) by Jaime Palomera (spokesperson for the Barcelona Tenants Union). This short piece looks at capacity constraints in relation to housing supply.

Michael I disagree with the implication and sentiment underlying your comment that “ The Taoiseach, many politicians and IIP etc. have made strong, public statements that make a direct causal claim about the impact of RPZs on supply. My fear is that their analysis will shape the public debate around RPZs, given their enormous public platform and substantial resources”

It is only in recent times that the perspective that seeks reform of RPZ has had even a modest representation in the public discourse. Any objective assessment will show that the media generally and consistently offers very generous space to so called housing experts and politicians (with the word expert being almost exclusively associated with not having any direct experience of residential development or working directly in the sector) who are strong proponents of current RPZ and or seeking to make it even more restrictive than currently …ie a rent freeze. I invite you to review media output on the topic of housing and it’s funding over the last few years and demonstrate otherwise. As regards IIP I am its only employee working from a home office, and if the assumption is that I preside over a vast organisation with limitless resources, then nothing could be further from the truth. The reason IIP was established was to belatedly give a modest voice to the perspective of our sector which deserves to be heard but which hitherto had no voice whatsoever with the debate on housing and its funding often dominated by voices utterly hostile to institutional investors usually relying in the main on polemic, prejudice, nasty name calling, mislabelling and dog whistling as a substitute for any real analysis or hard data to back up their argument. So why would you be “worried” that our voice might shape the debate? Are we not entitled to our point of view? Or is it a case of, to paraphrase a famous quote “ let every voice be heard, provided it reflects my point of view”

Hi Michael,

As someone who's a fan of your work, I'm disappointed by this post, for two main reasons.

Firstly, you call out the piece by Dermot, Michael and me in the Irish Times. The ad hominem that apparently Michael can only write things in his direct interest reflects poorly on you, particularly given the incredible amount of time that Michael gave, freely, to the Commission over the last number of years, to try to improve the housing system here. Being perfectly honest, I didn't think you'd stoop to such an argument - I had always thought of you as engaging with the substance, rather than the person. But reading this piece, you seem to link throughout particular messages with particular economic interests, which seems a cheap way of trying to 'win' an argument. I'm not arguing that we should ignore the source of the information (far from it) but you are trying to create a narrative here that would allow people with particular priors to ignore evidence that they don't like.

More substantively, you write that it is "quite remarkable that three members of the Housing Commission embarked on this solo run" to undermine its findings. Before this post, if you had asked me to name people who had actually read the Housing Commission report, yours would have been one of the first names on that list. As I would have said you knew, Recommendation #33, on rent controls, was the only one of the 83 recommendations that the Commission could not agree on fully. The op-ed by the three Commissioners unable to agree to the recommendation as it stood outlined that thinking in full, in particular in the context of a Sunday Independent front page story on rent controls a few days earlier, featuring the former chair of the Commission, that made no mention of it being the single recommendation where the Commission was unable to by unanimous. The op-ed that you disparage is, therefore, fully consistent with the published report of the Commission. This leaves us with two possibilities: either you read the report and are aware of this, but chose to misrepresent it above to strengthen your narrative, or else you have not read the Commission report in full.

My second main concern relates to the substance of your piece, as there are a number of problematic areas. In relation to how the PRS sector works, you would be far better served looking not at interest rates but instead at yields (gross or net) and how they have changed over time. There will of course be a link between the two, and of course both went up in the early 2020s, but one does not equal the other.

In relation to the analysis you have presented, it is somewhat haphazard and any instances of a fall in any one of investment, construction or starts are presented as evidence in favour of the conclusion that Ireland is not out of line. You note at the very start that "detailed posts like the below take a fair bit of work" but what I can't understand is why you didn't complete the work you started and develop a fuller understanding of the topic. If you had continued to assemble, say, CBRE data on residential investment, then you would have seen a very different conclusion to the one that you present.

For example, if you look at the volume of residential investment into the UK in 2018-2020 and compare it to 2023-2024, you'll see that the UK *increased* not decreased, and increased by 16%. The same is true of Spain. Investment has fallen in France, Germany and the Netherlands (and quite sharply in the latter two) but in none of those countries has the fall-off in investment been as sharp as in Ireland, where investment in residential real estate is down three quarters comparing 2023-24 with 2018-2020.

Surely academic curiosity would mean that you, as I, would be interested in what factors peculiar to Ireland might have driven that. What might Ireland have done differently than other countries? And it is here where qualitative and quantitative data combine. During this period, Ireland tightened its rent controls so that they are now certainly among the five strictest (and arguably among the three strictest) in the high-income world. I would recommend that you talk to those (without any connection to Ireland) that are still investing in residential real estate and who make the decisions about where to invest and ask them what has made them turn away.

In summary, we are in agreement that there a number of factors that have contributed to the decline in investment in rental housing, including the changed macroeconomic environment. And I fully agree with some of your final paragraph, in particular that "what bothers me most about all this is how high the stakes are, especially for tenants - the quality of our debate really matters".

But, you are not immune to that and it was "not at all difficult for me to find holes in the arguments" you have made against the hypothesis that tightened RPZs have impacted on the volume of investment in rental housing here. The single biggest determinant of rental affordability is rental supply and the single biggest barrier to rental supply at the moment is the poor state of our rent controls. This is a lever that, unlike the global macroeconomic environment, is in the control of policymakers here. Therefore, moving our rent controls to better align with those of peers makes sense.

Still a fan, just a disappointed one!